Some Thoughts on Things

ramblings on the current crypto & macro environment

as always, thanks for reading, follow me here and reach out at tolks@pageone.gg

The whipsawing, jawboning, mental insanity and, ducks, market manipulation will continue until morale improves. While working to finish this article before leaving for Spain and Portugal for two weeks tomorrow (what a time to be leaving the desk whoops), the headline terrorist struck yet again.

Markets of course rallied off the postponement of “planned military attack on Iran scheduled for tomorrow” but the major indexes, along with the coins, once again closed lower. So, where do we go for signal in a market that has never been more noisy? For me, as I stated on X May 9th, the signal comes from the macroest of macro assets: DXY, the US 10Y and 30Y and oil.

The easiest comparison of the current market environment to me is that it’s clearly 2021 but with the added bonus of a top-down, government mandated, manhattan project 2.0, singularity-god-chasing influenced market. While equities of course did incredibly well out of covid and into 2021, the main difference between now and then is that every marginal dollar of excess capital and liquidity is all flowing into the same AI trade. Instead of Axie Infinity or BAYC NFTs or watches or cars or countless, infinite tokens that could 5-10x, essentially every spare dollar is shoved into stocks.

The world’s most perfectly designed number go up market is seeing zero competition from any other capital or excess liquidity release valve. To me, this is one of the core reasons that the stock market not only feels, but is, so insane in recent months. The best argument for secondary capital capture is probably just ZEC, HYPE or pokemon cards but the scale of those tertiary markets is minuscule compared to the expanded risk curve of past bull markets. The AI trade is a liquidity black hole and the risk curve that benefits is directly downstream of that trade. And if you don’t want to take it from me, take it from a much more professional person, Danny Dayan.

“Only the Fed can stop what’s happening” is exactly what I outlined in that previously referenced May 9th tweet closing with, “inflation is clearly going to be a problem but until then/that announced pivot or one of these assets breaks it’s party on & melt up“. After a record-breaking rally from the Iran lows, the (potentially) bad news is, we’re getting real close to that breaking point and the market has given back some gains as a result. If anything can actually slow this market, it’s inflation + yields and they are, uh, looking incredibly not great. Horrendous even. Some charts and headlines to show that:

“Redbook sales goes from 7.8% YoY red hot to 2022 scorching hot 9.6% YoY in one week”

inflation moved up to 3.8% YoY in April, the highest level since May of 2023 as “rising energy prices are also increasing transportation, food and manufacturing costs, raising fears that inflation could spread across the economy and further weaken consumer spending.”

Copper prices reach a record high of $6.58 per pound, ground beef prices are at all-time highs, valuations & markets are of course at (or around) all-time highs

April PPI inflation surges to 6.0%, highest level since January 2023; Core PPI inflation rose to 5.2%, both CPI and PPI inflation are now officially at 3+ year highs

“The ‘Liz Truss moment’ of 2022 has turned into the UK’s political reality, with 30-year yields soaring to their highest levels since 1998 and the pound weakening. No matter who is in power, no matter their political leaning, there does not appear to be a credible plan to restore the country’s finances.” (this is spiraling and happening across the entire globe, not just the UK)

Auto loan delinquencies hit 32-year high as borrowers struggle with record payments

US credit card delinquencies hit 13.1%, highest since 2011; student loan delinquencies surge to 10.3%, highest since 2020; auto loan delinquencies hit record 5.6%

Japan long-term bond yields hit record highs amid fiscal concerns; Japan 40-year yield hits 4.41%, the highest level in history

“PPI jumped 1.4% m/m in April. Going back in the index’s history (to 2010), the only other month that saw a larger increase was March 2022.”

“South Korea’s stock benchmark Kospi index is on track to enter correction territory as rising bond yields threaten the world’s hottest stock rally driven by AI”

EU to cut growth outlook, raise inflation forecast as Iran war drives “stagflationary shock”

“China’s economy slowed across the board in April with investment resuming declines while retail sales and industrial output fell short of forecasts, underscoring the economy’s vulnerability in the face of a global energy crisis”

As with most things, the headlines begin to pile up after the market has already moved and boy have those four key assets moved over the past couple of weeks. The trend from the start of the year was already clear, but the fear these assets create has been put into hyperdrive since the hot CPI and PPI prints Tuesday and Wednesday. Markets initially shook the inflation numbers off, but as mentioned, have given back gains both Friday and today as digestion occurs. Importantly to me, and evidenced throughout the bullet points above, the inflation and yields problem is not US specific, but becoming a massive, global story.

In addition to those (bearish essentially all risk) assets having some of the best looking charts of any asset, we were also “due” for a pullback given the insanity of the rally from the lows. Some headlines that show this include:

“Roundhill memory ETF hits $10B AUM in only 30 trading days, surpassing IBIT’s record pace”

“April was the best month for the Nasdaq since Oct 2002, the bottom of the dot com bubble.”

“The only time the S&P gained more in a 6 week period is when the Fed launched QE1 after the global financial crisis.”

“S&P 500 breadth and price are on pace to move in opposite directions on 79 trading days this year, which would easily be a record since 1990”

So, now what tolks? Inflation is clearly scary and everything is up massively and yields and the dollar and oil look like they want to break out and absolutely rip. Well, first of all, I wish I had a definitive answer. Secondly, we always (try to) work in probabilities and to protect ourselves as much as humanly possible.

If you’ve been following my twitter, you know I’ve been bearish since the inflation numbers came out and am slightly worried about looking back on this moment in time as some type of true turning point. Yields are clearly yelling at the market and fed that they need to hike or entrenched runaway inflation might be here to stay. Scary.

But but but but! If I can deduce that information, the admin is surely aware of it. Two headlines last week that caught my eye further signaled this as, “Trump considering pausing the federal gasoline tax” and “in a bid to bring down record-high beef prices, the Trump administration plans to temporarily reduce tariffs to allow for more beef imports.” While I have no real idea what they’ll do (not helpful), I know for a fact they’ll do everything possible to continue the market rally and “combat” inflation by any means possible (that doesn’t include hiking rates). Solving the absolute clusterfuck that is the Schrödinger’s Strait of Hormuz is a great first step and I think the headlines today (of pausing further military action) are another admission of them attempting to do something.

Eventually, the market, yields or the fed specifically, may force their hand but until that occurs the party should continue. After all, it’s the Mahattan Project 2.0 and there is no outcome where we can lose the AI race to China. Again, it’s full steam (until you physically can’t) ahead.

In addition, I’m a full-blown believer in the entire AI thesis and, at least for now, the numbers and growth continue to support that outcome. The scaling and demand continue to be ludicrous for the time being. The earnings are great, the revenue is great, the constraints are real. The ever-increasing ceiling on valuations is real (for now). Just this week it was reported that Anthropic & SpaceX are once again raising the valuation bar higher ahead of their highly anticipated IPOs.

“Anthropic in early talks to raise $30B+ at a $900B+ valuation. Round could close by end of May. Valuation has more than doubled from $350B in February, when Google committed $10B and Amazon $5B with $50B in combined follow-on capacity. IPO reportedly on the table as soon as October. Surpasses OpenAi’s $852B March mark. Anthropic needs to make deals to pay for enough computing infrastructure to meet growing demand for its products, amid the breakout success of its AI software.”

SpaceX — approved 5:1 stock spilt ahead of IPO, will file publicly as soon as Wednesday. Roadshow as soon as June 4th, pricing as early as June 11th, Listing as early as June 12th. Seeking to raise as much as $75B at a valuation of more than $2 trillion, would make it the largest IPO of all time.

Moving forward, not hiking is the new cut and if we can figure out a way to cap yields, oil and the dollar, the result will be the same as when the top for oil and VIX were eventually put in. A mass chase and bid, both programmatically and through traders like you and I, that once again elevates stocks to new highs. The government mandated stock prices higher at all costs we need to build ai god will not go down quietly.

So, where that leaves me is, in a sense, so bearish I’m bullish? Consulting the bullet pointed list above about the global inflation and yield problems, combined with yet another TACO by Trump, is having me realize that the outcomes are kind of essentially The Big One or some form of pivot that further supports the market. In that scenario, 100 times out of 100, I’m always betting against The Big One. I haven’t wavered in the compute, memory and overall AI thesis yet and I don’t plan to until yields or the fed force me to.

As with anything in this day and age though, it is entirely fluid and unfortunately headline terrorism driven. It pays much more to be quickly reactive than to be predictive. While I came into writing this thinking I’d continue to be pretty wildly bearish, I think I’m going to fade that from here. With that being said, it is absolutely worth monitoring the four key assets I’ve harped about because if they do expand, we are going to really, really break some things.

Now, briefly before we get to the coins, I would like to posit my thoughts on the endless bubble or not bubble talk. The debate is wildly complex with good arguments on both sides, but the conclusion is much simpler. If I own the asset, it’s not a bubble and you should buy it immediately. If I don’t own the asset? Well, it’s absolutely a bubble and you should watch out below.

Cryptographic Currencies

After a close to two weeks long fun, profitable tenure on the bull train I unfortunately find myself leaning back in the bearish crypto camp as of writing. I shorted BTC, ETH and SOL on Tuesday morning after the inflation print and added some more following the PPI print that was released Wednesday. In addition to that, the clarity act bid and the latest STRC dividend date bid have now come and gone and we’re left with a confusing mess of underperformance.

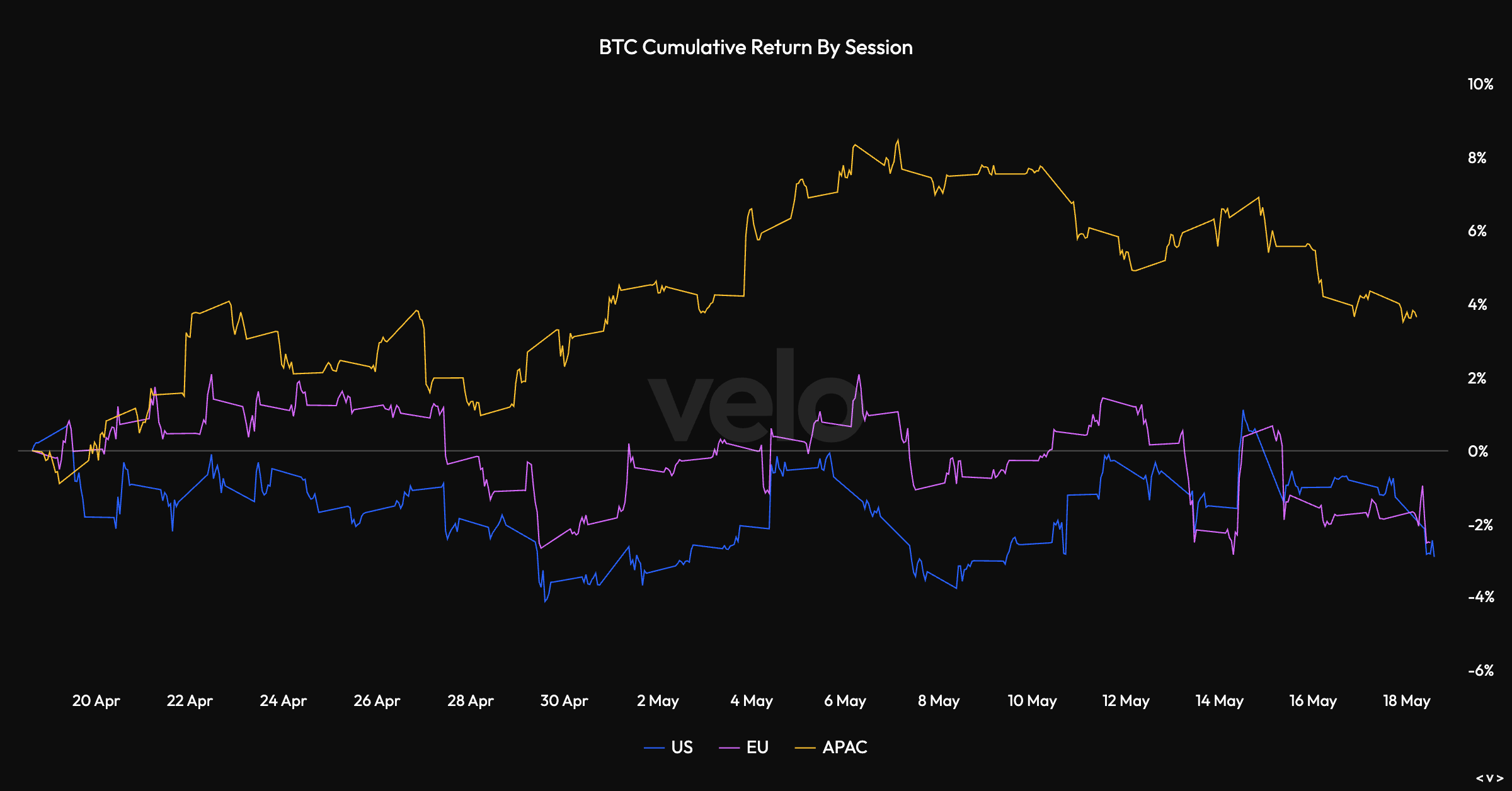

As I wrote throughout the above section, the macro picture is messy, scary and confusing but also so bearish it’s bullish? I don’t think there’s really any scenario where coins, outside of ZEC & HYPE ofc, catch a meaningful, sustained bid downstream from the liquidity black hole that is the AI trade. Unfortunately, as the above image suggests, that has left me often times using the coins as short hedges to my AI exposure. (As of writing, maybe against my better judgement, I have actually closed those shorts at ~77k, ~2140 & ~85. This is partially because I’m traveling for two weeks tomorrow and partially because it kind of feels right given the current TACO and downside we’ve seen. I’ll be quick to add back if the so bearish I’m bullish idea fails.)

As a wise man on Twitter wrote weeks ago, “we’re in the early stages of a new Industrial Revolution and crypto doesn’t really align with it. Much of it looks like inefficient capital allocation. There’s one (+ tome lee) deranged guy buying hand over fist while everyone else is focused on a different game. I’ve said this before, the dynamic doesn’t shift until there’s a deeper correction that triggers a meta shift.” The above Velo image on BTC returns during the US session, along with the lack of excess capital flow I detailed earlier, perfectly highlights that quote. Crypto, again outside of HYPE, ZEC & a few other select coins, is just an uninteresting use of capital for the time being (I still hold plenty of BTC, HYPE & ZEC and add more weekly but most everything else is limited to a trade instead of conviction).

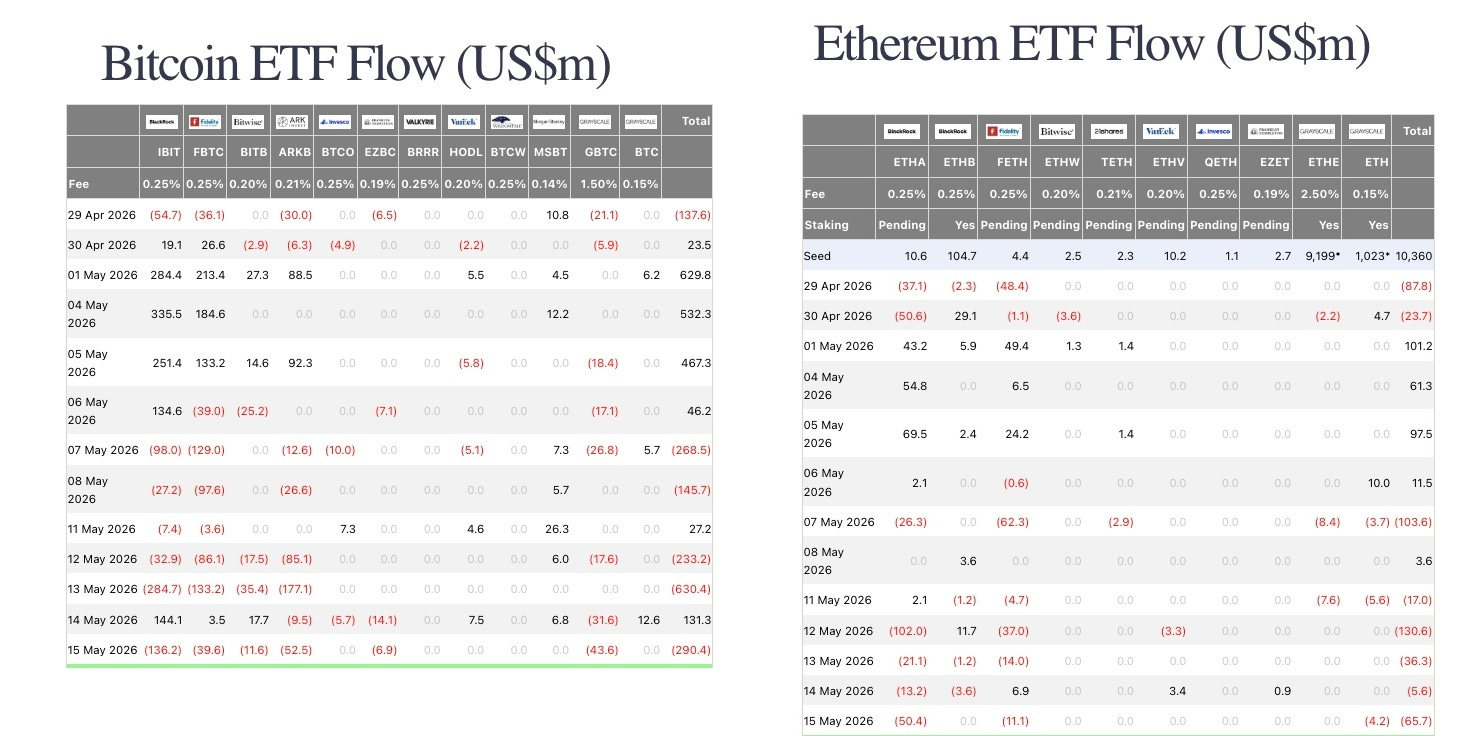

It pains me to write that, but 1) I am simply the observer and messenger of what the market is telling us and 2) nothing lasts forever. For now though, outside of the market anointed good coins, the rest of the market, BTC included, is fighting for it’s life inside the AI vortex. Additionally, and further support for the AI black hole thesis, the ETF flows have been putrid while stocks have generally continued higher in recent weeks and we’re actually now seeing somewhat meaningful outflows.

Even with the shorts now currently closed, I have an incredibly difficult time envisioning any form of a sustained bid for the majors (BTC, ETH & SOL) and the never-ending supply of alt coins fighting the uphill Sisyphus push of monthly token emissions. It certainly doesn’t help those coins that Saylor has signaled the potential of BTC sales, last week bought $2 billion worth of BTC at an average price of ~80k for the chart to look how it does (spoiler, not great), SOL’s identity crisis while memecoin trading is mostly still in the gutter and Tom Lee saying they’re “gonna slow down our pace of buying (ETH), because there’s other things to be doing in crypto right now.” Not great for those assets and exactly why I choose them for my short hedges when deployed.

As always, with the gluttony of bad news out of the way, let’s talk about the good. Hyperliquid. Zcash. VVV. On various occasions numerous other alts (AKT, TAO, TON, LIT, MON, NEAR, CARDS, etc.). While the picture is relatively bleak for BTC, but more specifically ETH & SOL, it’s never looked better for other coins (again, specifically HYPE & ZEC for me).

The ability for some coins to create their own narrative and bid while BTC, ETH and SOL generally look like dogshit is a welcome surprise. I think this is ironically partially because the AI vacuum exits. It’s never really been easier in crypto to employ long/short strategies in a confident manner. There’s also a mechanism where crypto is generally starved of capital, again weighing primarily on the majors, so the good coins and the capital available quickly identify what is underpriced, strong, momentum filled and good.

When you zoom out on various charts, there are clear, wild differences in structure between coins such as HYPE, ZEC and VVV compared to BTC, ETH & SOL. This is not only healthy for the future of crypto (unique assets getting idiosyncratic bids), it creates an environment where even when the majors are weak there are undervalued tokens that reward people with conviction in good tokens. I continue to think this will be the case moving forward and the most valuable use of your time in crypto is searching for undervalued alts that could be the next HYPE, ZEC, VVV, etc. That is of course easier said than done, but the opportunities are out there.

This crypto section is admittedly a bit shorter than usual but it’s a function of the current environment outlined, how insane tradfi has been and the endless talk about HYPE & ZEC on CT to where it seems repetitive to spew the same things that have been a core focus there for weeks. They’re good coins! Some other headlines that caught my eye in recent weeks are listed below. I’m off to Spain and Portugal for two weeks tomorrow so I’ll be less active on Twitter and here, but expect another post when I’m back and fully caught up on things. Cheers, friends.

Morgan Stanley launched its crypto trading offering via E*Trade to a subset of customers, undercutting Coinbase, Robinhood, and Schwab on transaction fees, with a 50bps take rate.

Charles Schwab officially launches spot crypto trading services for retail in US

Jez introduced papertrade_xyz, “a fair-launched, fully-onchain perpetuals exchange built on hyperliquid; 1000x leverage, 0 slippage, no funding costs, self-bootstrapping LP

Clarity Act clears Senate banking committee hurdle

Western Union launches USDPT stablecoin on Solana

Circle raised $222 million in the presale of a token tied to its new Arc blockchain, giving the network a fully diluted network valuation of $3 billion

SEC is said to ready plan for trading crypto versions of stocks

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions.

Thanks. Great read to capture the overall sentiment and the road ahead.