What The Futarchy

Examining the voting machine & the inefficiencies of the market

This article was submitted as part of the Solana Scribes; Content Hackathon

As always, thanks for reading! Follow me here and reach out at contact@pageone.gg

In Economics, a popular concept known as the “Efficient Market Hypothesis” (EMH) is a controversial idea. It states that "share prices reflect all available information and consistent alpha generation is impossible.” In theory, stocks always trade at their fair value on exchanges, making it impossible for investors to purchase undervalued stocks or sell stocks for inflated prices.

While there is ample academic evidence to support the core theory, there is equally as much “free market” evidence that discredits the EMH. As a crypto market participant, I of course fall into the latter camp as inefficiencies are as abundant in crypto as arguably any asset class in history. Crypto is also (clearly) an asymmetric bet on a better, more efficient internet and monetary system despite what the European Central Bank or Elizabeth Warren would desperately claim.

Asymmetric bets, by their very definition, can’t be efficiently priced. At the core of this idea lies the main problem; how is the ‘information’ viewed by the participants? We all know the phrase ushered by John Maynard Keynes, “The markets can remain irrational longer than you can remain solvent.” This opens up a brand new dynamic set of questions:

What dictates how the participants in the market view potential news?

How long are you willing to wager on a “mispriced” asset?

How long can you remain solvent against the herd of the markets?

The market is essentially a living and breathing being. Despite endless efforts from a countless number of the world’s smartest and wealthiest people, the markets continue to evade anyone who tries to codify and understand its abnormality. These same “inefficiencies” pose problems in being represented by models and have turned the markets into what is lovingly referred to as a “PvP Arena”; The winner of which profits in an outsized way.

One of these PvP arenas is prediction markets which are open markets that enable the prediction of specific outcomes using financial incentives. Prediction markets, more colloquially known as betting markets, allow anyone to quite literally put their money where their mouth is on various topical things ranging from everyday sports events to political elections and even the outcome of wars. Due to how you take part in prediction markets (financial stake + reputation) only those knowledgeable in the said sector or “experts” of their communities are attracted here (or at least, that’s the consensus).

There is a growing merit to the idea too. Traditional means of “information seeking“ aren’t usually monetizable beyond the sector you’re a part of. In prediction markets, if you spot an inefficiency and have the relevant knowledge, you can win big. Secondly, because of said structure, the scope & breadth of information represented in the markets also rises significantly. This is evident in the US Election forecasting data study conducted by David Rothschild where he looked at the 2008 presidential elections.

In it, expert forecaster Nate Silver was pitched against the Iowa Electronic Markets (IEM). Nate had built his model from more or less general polling data but the IEM didn’t have information restrictions. As a result, the IEM incorporated information from wherever they found useful while also addressing any biases they felt were present in Nate’s model ultimately leading to the IEM performing better.

Prediction markets however are heavily regulated (due to their financial nature) and there is only “so much” you can create markets on in that framework. Luckily for us, crypto is the test bed of innovation and this remains true for prediction markets too.

As it currently stands, Polymarket is the biggest prediction market in the world that hosts everything from crypto and politics to even pop culture and war outcomes. However, given the nature of prediction markets and seeing what they can potentially power, to leave it at just betting over “which main character gets arrested by Q4 2025” isn’t the best implementation of the tech.

The ramifications and potential of prediction markets grow when you see the results of prediction markets’ ability to accurately represent real-time events to a high degree. We’ve even seen Prediction Market Dating and to kick things up a notch more, in the most Silicon Valley Tech Bro move I’ve personally seen, “The Prediction Market Dating Show” which describes itself as “a surreal musical odyssey of romance and live betting”.

When we’re not focused on these edge cases and want to make better use of the underlying market system, this is where Futarchy comes in. Proposed by Robin Hanson as a futuristic form of government, the one-liner explains the idea perfectly:

Vote Values, But Bet Beliefs

The idea builds upon the core premise of these information markets with a slight twist. This is called “Conditional Prediction Markets”. Individuals would not vote on whether or not to implement particular policies, but rather on a metric to determine how well their country (or charity or company) is doing. Then, prediction markets would be used to decide the policies that best optimize the metric.

Given a proposal to approve or reject, two prediction markets would be created each containing one side of a market corresponding to acceptance of the measure and one to rejection. Depending on which market wins, the losing market will have their trades reverted and depending on the metrics of the winning markets, the trades will be paid out accordingly. Due to the nature of this system, the measure of success or “perceived value” is evident almost as quickly as the markets are created.

Prices in prediction markets reflect the probability of an outcome. So if the pass market has a price of $0.75 per share for Option A and $0.25 for Option B, this is the market telling you that they believe Option A has a 75% chance of winning. This is the main premise of Futarchy. Traditionally in governmental voting, you have "voter apathy" and "rational irrationality" but Futrachy aims to have a much more rational market which incorporates all kinds of information.

Secondly, due to the financial nature of reducing these irrational inefficiencies, over a longer period, these markets will weed and filter out participants who have a “higher % win rate” vs lower, which forces the participants to evolve. In gaming terms, think of a prediction market in its early days as your “placement matches”, where you play against players with all kinds of skills. However, the more you win and grow, the more you get placed with other players of a similar calibre which evens the skill ceiling and makes the game more competitive. The same principle applies here.

In theory, this seems to be the perfect blend of “public” participation and professional analysis, however, there is a downside to this model which may be big enough to outright not make this model work.

Should a single person (or entity) want to manipulate the markets, they can with an obscene amount of money by pushing the prices they want of “yes” and “no” in their favour. Then we have the issue of the financial nature of these being a double-edged sword. All markets by nature are “reflexive”, the buying of an asset goes up when we see others buying it too. This is very evident in crypto with phrases like “Monkeys Ape Together”, the practice of “Whale Wallet Tracking” and even “Influencer Shills”. While the premise of Futarchy is based on rationality, the participants are anything but and this “gap” between the two also leaves the door open for manipulation of the markets.

Secondly, and this is something which I resonate with, it’s very hard to differentiate between the “noise” and the actual impact of a policy being implemented, especially on a longer-term scale. If you were around for the “WAGMI” era of crypto last cycle, you will remember this music video from Randi Zuckerberg.

This is what being 100% engulfed inside of an echo chamber looks like, where the noise can not be differentiated between the actual impact long term. While you may have the “more rational” participants betting on the correct outcome, the noisy crowd can make that vote fail and we wouldn't have known until 2-3 years later that “WAGMI” wasn’t the best of ideas. My good friend Poof has been working on analysing the insanity that was the 2021-2023 period of NFTs which looking back just goes to show how hard it is to differentiate from noise. Check it out here:

In the beginning, I mentioned “how is information” perceived, and this gets translated further. In my previous article, I mentioned that growing up through the schooling system in the UK is heavily contrasted with that of the US (through the lens of school uniforms) and this can be expanded further. Not only will there be differences in the consensus of how that information is perceived, but there is also going to be equally as much debate into how that information or “metric” is captured. Any policy can be made to look good using the right metric after all.

This also leads to a situation whereby more manipulative participants, adopting tactics like the “Motte and Bailey Fallacy” become a concern.

[The Bailey] represents a philosophical doctrine or position with similar properties: desirable to its proponent but only lightly defensible. The Motte is the defensible but undesired position to which one retreats when hard pressed.

Finally, if you’ve been paying attention, you’ll also have realised that prediction markets are a zero-sum game. By design, it’s irrational for you to participate in them. What this situation leads to is the participants who are willing to participate are not going to be experts but rather speculators who *think* they can trade on what the markets expect not what they believe will happen. This is referred to as a Keynesian beauty contest; judges are rewarded for selecting the most popular faces among all judges, rather than those they may personally find the most attractive.

Between these pros and cons and the matter of money involved, you’d usually be hard-pressed to find a system like Futarchy implemented “in the real world” but luckily for us, we can experiment with ideas like these to see if they’re just good on paper or do they scale?

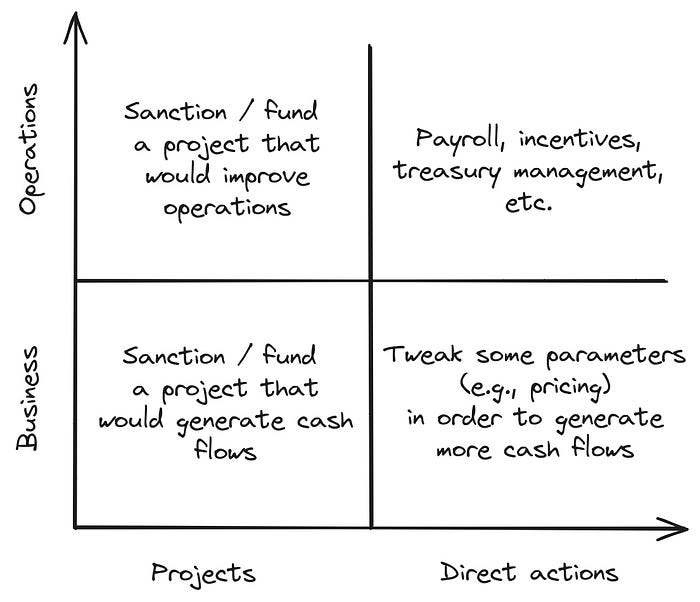

Meta-DAO wants to put the idea and implementation of Futarchy to the test and we’ve already seen some interesting results come from it. Proph3t (Co-Founder of Meta-DAO) posted an interesting case where he wanted Proposal 3 to fail for his profit and outlined all the ways how he could’ve manipulated the markets to reach his goal. They have big ambitions too. In their introductory post, they envision business proposals and operations proposals along the area axis with the scope axis containing projects and direct actions.

Interestingly to me (as this only cleared a few days ago), was the failure of Proposal 9. Agrippa (The proposer) outlined his vision and execution plan for implementing “multi-modal” support. As of writing, Meta-DAO only supports “Yes” or “No” markets, and this proposal passing would’ve allowed for multiple “mutually-exclusive outcomes, one of which is fail and the rest of which are other things.”

This would’ve been a huge quality-of-life addition to the DAO as the proposals would no longer be “binary” along with more nuance in the prediction markets of different implementation odds too. He talked about what the value add would be for the DAO, his qualifications, how he talked to the Proph3t in person about this, and gave a brought time scale with “trenches” on him hitting deadlines before the compensation was given to him. Yet, it didn’t pass. Why? Because the compensation he set for himself was too high as he didn’t want to be paid in USDC, he wanted to be paid in $META.

Considering this from Agrippa’s perspective, I would argue that he was rational throughout. He possesses the relevant skillset, a clear value add for the DAO, recognised the connection between the two and then took a speculative gamble on getting paid in the governance token rather than $USDC (profiting highly if it goes up but also losing a lot more if it drops below). However, when I looked at the discussions happening *within* the discord server during this, the overall sentiment was this “We like the idea but because you’re asking for compensation in $META, it means you get paid a lot more than others usually will.”

The image below was Proph3t’s response to the proposal which I would say is quite rational as well. What is there to stop someone else from coming in and bidding a marginally lower "compensation package” and underbidding Agrippa? Nothing, but at the time of writing, no one else has come forward with a similar proposal to build a multi-modal system.

This is why I find crypto fascinating. The idea of Futarchy has been around for over a decade and while it’s been talked about and debated, no one has built out this system. In crypto, you can put these ideas to the test and see first-hand how *actual, global* participants will react. Earlier I mentioned that I don’t personally believe in the Efficient Market Hypothesis (despite having a Masters in Economics) and this is why; it never considers the human aspect of who is behind the screens. In crypto, the *only* part I would argue that lasts and is memorable is those exact human elements.

This is one such experiment of that “human element” meeting “professional analysis” and I think it’s going to be an interesting one to keep an eye out on for that mix alone. This is the future I’d love to see in the space, that of unbridled experimentation.

If you’ve made it this far, thank you for reading and I hope this has been a useful read. You can follow me on Twitter (and now Farcaster) to let me know what you think about this post & don’t forget to subscribe to Page One for your essential crypto readings!