as always, thanks for reading, follow me here and reach out at contact@pageone.gg

tl;dr: CZ steps down, inflows continue increasing, Blast engulfs $580M, SOL activity keeps climbing, ETFs are imminent, GBTC discount collapses, & clear skies ahead

BTC dominance 53% | ETH dominance 18% | DeFi TVL $46.2B |

Total Crypto Market Cap $1.47T | Stablecoin Supply $128B |

If there was a singular word to describe crypto in 2023, cathartic is deserving of the crown. Three weeks after SBF was found guilty on all seven counts the DOJ charged him with, CZ pled guilty to violating the Bank Secrecy Act and has stepped down as CEO of Binance. One of the last remaining dark clouds from last cycle’s blunders is now cleared.

The tl;dr on the consequences for both CZ and Binance come from wolf and include: CZ personally fined $50M, no involvement in Binance operations for at least 3 years, Binance appoints an independent compliance monitor for 3 years, Binance fined $1.805B paid over 15 months + $2.51B for sanctions. As for where they go from here, CZ has paid his $175M bond and awaits sentencing (where he could face up to 18 months in prison) on February 23rd and Binance has appointed Richard Teng as its new CEO.

What began with the DOJ investigating Binance in 2018 has finally come to a rather (thankfully) anticlimactic ending as the agreements from both CZ and Binance settles ongoing investigations from the DOJ, Treasury, & CFTC. According to DeFiLlama, Binance has seen $1.94B of outflows over the last 7 days. Still, Binance has $66.5B worth of assets, has (so far) quelled any insolvent rumors, continues normal operations and has maintained a dominant/normal share of trading volume.

As previously mentioned, the DOJ’s years long investigation into Binance provided some hesitancy for market participants across the entire spectrum, from crypto natives to institutions. Eventual outcomes were scattered, ranging from a slap on the wrist fine to the tail risk, worst case scenario of a full shutdown and seizure of Binance. While one can philosophically argue CZ’s punishment isn’t deserving, the terms of the settlement are about as good as possible for the future of crypto. As JPMorgan notes, the settlement eliminated “potential systemic risk emanating from a hypothetical Binance collapse”.

For years, there’s been not so subtle whispers of displeasure for CZ/Binance from some of the largest financial institutions and politicians in the U.S., a qualm that has now been resolved. With the settlement official and Binance back to essentially normal operations, there are clear skies and abundant catalysts ahead for crypto.

Of those catalysts, BTC’s eventual spot ETF approval is of course paramount as it continues to drive crypto prices upward. Everyday that passes, we’re almost certainly one day closer to approval with the last possible target date remaining the same as it has since October. That date, January 11th, is the deadline for a final decision on ARK’s application and is suddenly a short 44 days away. While I’ve written about likely approval before that date since ~October 1st, the recent verdicts against SBF, FTX, CZ, & Binance clear the arena for an even greater chance of approval as regulators have “cleaned” up crypto to insert their friends (Blackrock, Fidelity, VanEck, etc.) through ETF approvals.

Furthering that thought was a week of “bullish discussions” as the tradfi giants have had continued back and forth dialogue with the SEC, something that never previously happened. As our ETF friend James Seyffart says, “Grayscale had meetings with the SEC’s division of trading and markets (the division in charge of approving or denying 19b-4s). Have also heard rumblings of other potential spot BTC ETF issuers meeting with SEC in last ~week or so.” Later, James further comments on the reports of discussion between applicants and the SEC saying, “events of the last few days haven’t changed our odds. We can’t go higher than 90% by January 10th. That said, things are continuing to move forward in our view.”

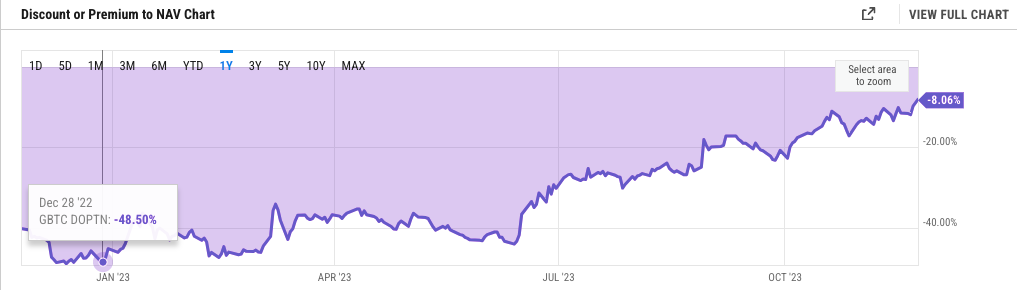

If Bloomberg ETF analysts and settlements with Binance/CZ can’t convince you of imminent ETF approval, maybe the GBTC discount chart will. As recent as June, the GBTC discount was near its all-time lows sitting at -44%. Since then, the discount has continually shrunk signaling that spot BTC ETF approval & GBTC redemptions are fast approaching (only possible with GBTC’s conversion to a spot BTC ETF).

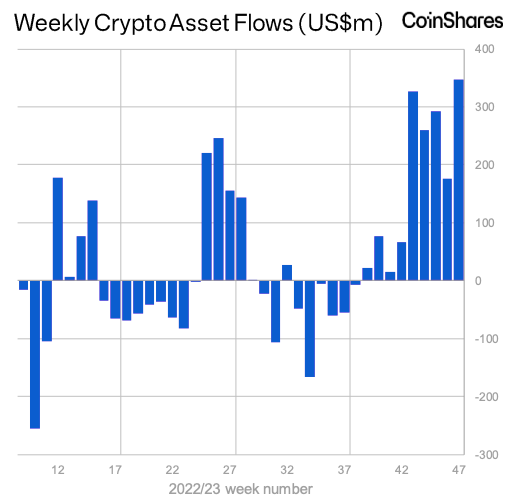

In addition to the GBTC discount shrinking, the future catalysts growing, & the potential Binance dark clouds eliminated, inflows continue to support the recent price appreciation. CoinShares notes that last week, digital asset investment products “saw inflows totaling $346M last week, the largest weekly inflow in this 9 consecutive week run…this run is the largest since the bull market in late-2021.”

Combining the slow but steady growth in stablecoins, the CoinShares Digital Asset Fund Flows report, the ever-growing volume of the CME & COIN’s recent strength add support to the likeliest scenario of spot ETFs being approved anywhere from now until January 11th. Specifically, the continued fund asset inflows, GBTC’s decreasing discount & CME volume signal that almost all of the recent price appreciation has come from a barbell of institutions positioning as best they can ahead of the ETF approval combined with the surviving crypto natives deploying capital. The era of CZ running Binance has come to a close, but the future of tokenization & crypto growth has never looked better.

Outside of CZ & Binance, the other major topic of the week was Blast. Blast is currently, “the only Ethereum L2 with native yield for ETH and stablecoins.” Opinions on the latest “L2” have resulted in chaos on CT as responses to the yield farm they launched have people incredibly divisive. The L2/bridge quotations are worthy imo as it currently stands, and will be for the foreseeable future, the Blast “bridge” & “L2” operate as a one-way transfer of funds to a multisig generic contract on ETH.

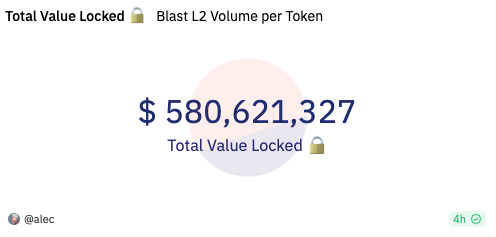

That multisig generic contract has CT in a frenzy largely because of the GTM ponzification and capital sink it has grown to. As of writing Monday night, Blast’s TVL has reached a staggering $580M+ in a ~week. Assets bridged consist of $361M of ETH, $139M stETH, $35M USDC, $26M USDT, & $15M DAI.

As essentially everyone is aware of, we’re firmly in the era of magic internet points accumulation in the hopes of a future translation of points to magic internet money. While often times the farming/yield/reward of eventual magic internet money is obfuscated, Pacman and the Blur team have consistently done an incredible job of leaning into, not hiding, this taboo through clever mechanism & token sink design.

Blast’s outlined design, an L2 where bridged ETH & stablecoins earn native onchain yield through the ETH staking rate + RWA assets (stablecoins deposited into protocols like MakerDAO generating real yield from T-Bills) is genuine innovation that benefits both bridged capital and the attraction of TVL to Blast. Expect established L2s to eventually incorporate similar mechanics and Blast to be the first of countless future L2s/L3s experimenting with yield + mechanism design to attract idle capital.

With that being said, Blast is not without its faults. First, the L2 and bridge they boast are, until proven otherwise, entirely theoretical. Currently, the ~$580M of “bridged” assets sit in a generic contract on the ETH L1 as the Blast team continues to build the promised functionality of their future L2. Secondly, the mainnet launch of their future L2 isn’t until February of 2024 when the “bridged” assets will be available for withdrawal and native dapps are live. Those assets ($580M worth mostly in ETH) are locked until ~3 months from now with the eventual redemption of the accumulated magic internet points not converting to Blast tokens until May of 2024.

While the decision of market participants to bridge and lock assets for ~3 months can’t be judged until the yield generated through future Blast tokens is clear, we have some core learnings in the present. Those to me are:

Embracing (relatively) Sustainable (“riskless”) Yield — Blast is the first, but it’s inevitable that we see already established + future L2s embracing/building upon the concept of dollars onchain earning yield being a net goood

L2 Experimentation — with Blast launching, and the ability to fork existing L2s and/or launching your own rollup growing easier by the day, we’re destined to see the increasing ponzification of L2s similar to what we saw with last cycle’s L1s

Mechanism Design — despite the pleas for “professionalism” from some crypto investors, the entire space is ~10 years old; DeFi is ~3 years old and anyone telling you outcomes are certain is drastically mistaken; experimentation and net new designs like Blast should be criticized for their flaws but broadly welcomed

Idle Capital — as mentioned, over the course of the last ~week, $580M worth of assets have been bridged to Blast; as we exit the down only stages of the last ~2 years, it’s clear that there’s a massive pool of idle onchain capital ready to generate yield + potential future rewards

The resulting effect of Blast, positive or negative, will unquestionably be criticized but the growing experimentation of mechanism design is certainly a welcoming site. The eventual hindsight analysis is of course flawless, but crypto was quite literally built for permissionless development and the Blur team deserves credit for consistently being at the forefront of experimentation.

As usual, there’s too many core developments to cover in depth so the following items fell below the fold but remain incredibly important moving forward. These include:

BTC fees & Ordinals — as brc-20s & Ordinals continue their renaissance leading to BTC fees on November 16th exceeding the total fees paid on ETH for the first time since December 2020; as I’ve written previously, anyone expecting the previous spike in attention, fees, & maturation of Ordinals to pass by as a quick fad is mistaken; they’ll continue their growth throughout 2024 & beyond (s/o Udi & the Taproot Wizards forever and always)

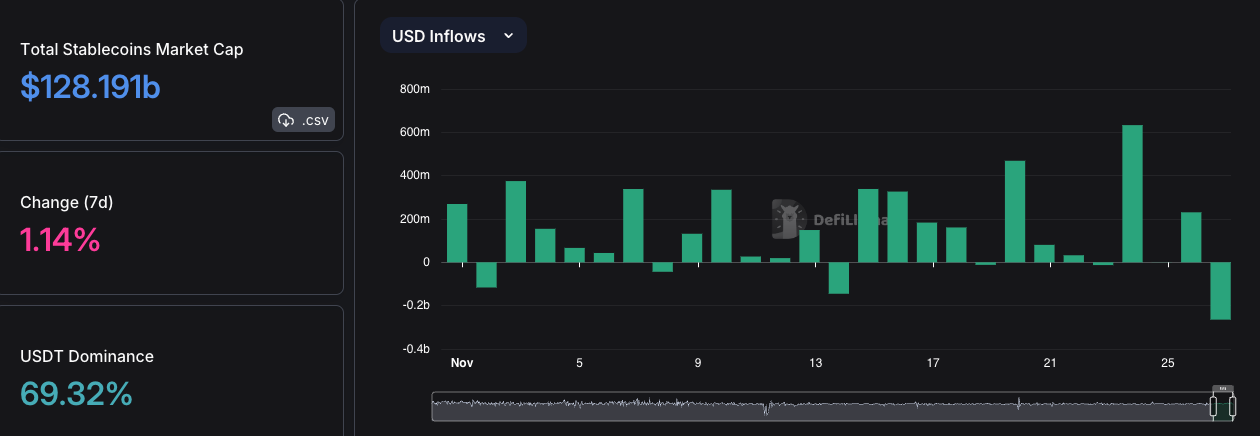

Steady Inflows — stablecoin inflows, while mostly benefitting USDT & FUSD, have gradually climbed higher throughout November as the stablecoin total market cap has climbed from $124B to $128B+; additional inflows can be seen from the CoinShares data linked earlier as digital asset fund flows have increased for 9 straight weeks bringing 2023’s fund inflows to a total of $1.66B

image from DeFiLlama stablecoins overview Oracles — SOL-based PYTH has successfully completed its long-awaited token airdrop while LINK (ETH-based) staking v0.2 will go live Tuesday at noon EST. LINK remains far and away the dominant oracle by TVL while PYTH has rallied ~50% since its airdrop claim lows. PYTH’s circulating supply remains low for the next ~5 months so we’ll likely see PYTH’s market cap ($623M) gain ground on LINK’s ($14B) over the course of the next few months. Oracles have been and will continue to be a critical part of all things crypto/DeFi and LINK/PYTH should display good beta to ETH & SOL

ATOM — Cosmos Hub governance approved a proposal to reduce ATOM’s max inflation rate from 14% to 10%; Additionally, Circle’s CCTP for USDC will be live on Noble, the asset-issuance chain in Cosmos, this week. “CCTP will allow anyone on ETH, AVAX, ARB, Base, OP, ATOM & soon SOL to directly move USDC natively into DyDx without bridged or wrapped USDC.”

GBTC — the discount to NAV of Grayscale’s flagship GBTC product is currently below 10% for the first time since 2021, adds further confidence to the SEC’s approval of spot BTC ETFs before ARK’s deadline on January 11th. ETF approvals are unquestionably bullish mid-to-long term but JPMorgan (as well as plenty on CT) say GBTC could eventually see outflows of $2.7B upon Grayscale’s conversion of GBTC to an ETF, would stem from speculators who bought GBTC’s discount redeeming their purchases for the underlying value upon conversion

Phantom — SOL-based wallet debuts Cross-Chain Swapper & Refuel. The CCS enables the bridging of tokens across ETH & SOL natively in Phantom. Refuel enables users to convert a portion of their bridged tokens to SOL so users can instantly pay for transactions as soon as they bridge. Phantom’s CCS & Refuel are another example of UI/UX/onboarding issues of previous cycles slowly being solved natively in dapps & wallets.

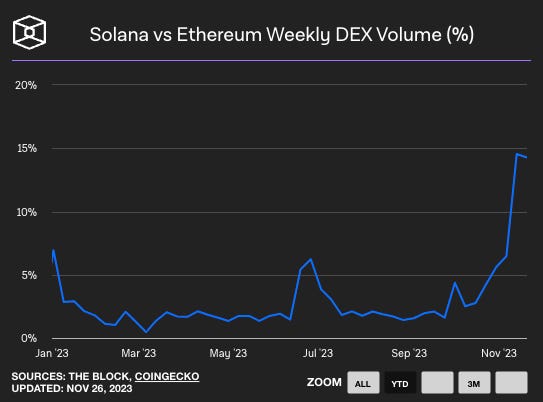

SOL tokens — while I’ve been writing about this scenario for months, SOL ecosystem tokens have exploded over the past few weeks; most have given back some recent gains, but the looming Jupiter, Jito & MarginFi airdrops provide support; the number of biddable SOL tokens/ability to profit from them has long been a gripe of CT but that has and will continue to change as it becomes a massive plus where every future bridged + airdropped dollar has a small concentration of tokens (10-20 max) to rotate funds to; SOL/ETH weekly DEX volumes + SOL DEXs reaching new volume highs further illustrates the point

As a reminder, the P1 team is always reachable at contact@pageone.gg. If you want to sponsor the newsletter & reach an audience of 12k+ active market participants, pitch a guest post, tell us about your protocol or to collaborate on anything in general, you can always reach us there or @PageOneGG.

funding:

Phoenix Group, UAE-based BTC mining/service provider, raises $370M in IPO

Drift, SOL-based onchain cross-margined perp protocol, raises $23.5M Series A

Blast, ETH L2 w/ native yield for stablecoins + ETH, raises $20M

Privy, infra company that led the PWA mobile app growth, raises $18M Series A

CFX Labs, SOL-based stablecoin payment/remittance protocol, raises $9.5M seed

Panoptic, perp options DeFi platform, raises $7M seed

OMTrade, social trading platform, raises $6M seed

news:

SEC again sues Kraken, alleges they’re operating as an unregistered online trading platform; SEC delays decision on Hashdex Nasdaq ETH ETF application

UK Treasury approves tokenization for UK investment funds, cites potential of tokenization to “improve efficiency, transparency, & international competitiveness”; UK finance minister also announced legislation to boost the nation’s digital asset sector

Republic to launch tokenized investment fund Republic Note on AVAX, aims to generate profits from 750+ private assets & has received $30M in pre-sale participation

Mt. Gox to start repaying creditors in cash before year end & throughout 2024

Pro-BTC populist Javier Milei wins Argentina’s presidential election

Crypto exchange Bullish acquires CoinDesk from DCG

CoinGecko acquires NFT data startup Zash

Open interest for BTC options on Deribit reaches ATH of $15B+

tokens & protocols:

LINK — staking v0.2 launches on Tuesday, comprehensive overview here

SOL — TPS now regularly surpassing 1k non-voting transactions

COIN — Coinbase stock climbs to $115, highest price since May 2022

ATOM — governance passes vote to reduce ATOM inflation from 14% to 10%

AVAX — Republic Note to launch tokenized investment product on AVAX

PYTH — SOL-based oracle service distributes highly-anticipated airdrop

SYN — Synapse bridge adds support for bridging to & from Solana

DOT — launches $45M grants program, outlines major updates for Q1

KNC — KyberSwap suffers exploit, hacker steals $47M

EigenLayer — launches stage 2 testnet: EigenLayer & EigenDA

Jupiter Exchange — adds Linea, Base, OP, & Tron to bridge comparator

Backpack — SOL-based wallet & xNFT creator debut their in-wallet exchange as simple trading of SOL/USDC is now live

around the ecosystem:

0xKofi introduces GPT-powered DeFi data analyst “DeFiLlama GPT”

Joel John on “The L2 Paradox: or why a lack of users leads to rising costs on L2s”

Austin Barack’s “Reflecting on Breakpoint 2023 and the State of Solana”

ZeePrime Capital’s excellent read “RWA vs NWA”

tweets:

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions.

Great work once again 👏🏻